The CIA integrates AI assistants, Bitcoin hovers at $72K, and the RWA market outlook turns bullish; meanwhile, the crypto market rebounds from extreme fear with USD 250 million in short liquidations. Today’s crypto market showed a notable recovery as weak macroeconomic data and shifting geopolitical developments set the backdrop. Bitcoin fluctuated around the $72,000 level and helped lift broader market sentiment. The latest market data showed that total liquidations across the crypto market reached USD 342 million over the past 24 hours, with short liquidations accounting for a dominant USD 250 million. This suggests that a broad short squeeze was triggered as prices moved through key resistance levels. At the same time, U.S. equities remained strong, with both the S&P 500 and the Nasdaq Composite posting gains for a seventh straight session. That sustained rally in stocks provided a supportive external setting for risk assets. Although negotiations between Israel and Lebanon improved expectations for geopolitical easing, investors remained highly focused on inflation data and recession risk. Overall, the market appears to be in a rebound phase after an extremely depressed sentiment stretch, while sectors such as SocialFi and Layer 2 outperformed the broader market and showed a more concentrated flow of capital.

Crypto Markets Overview

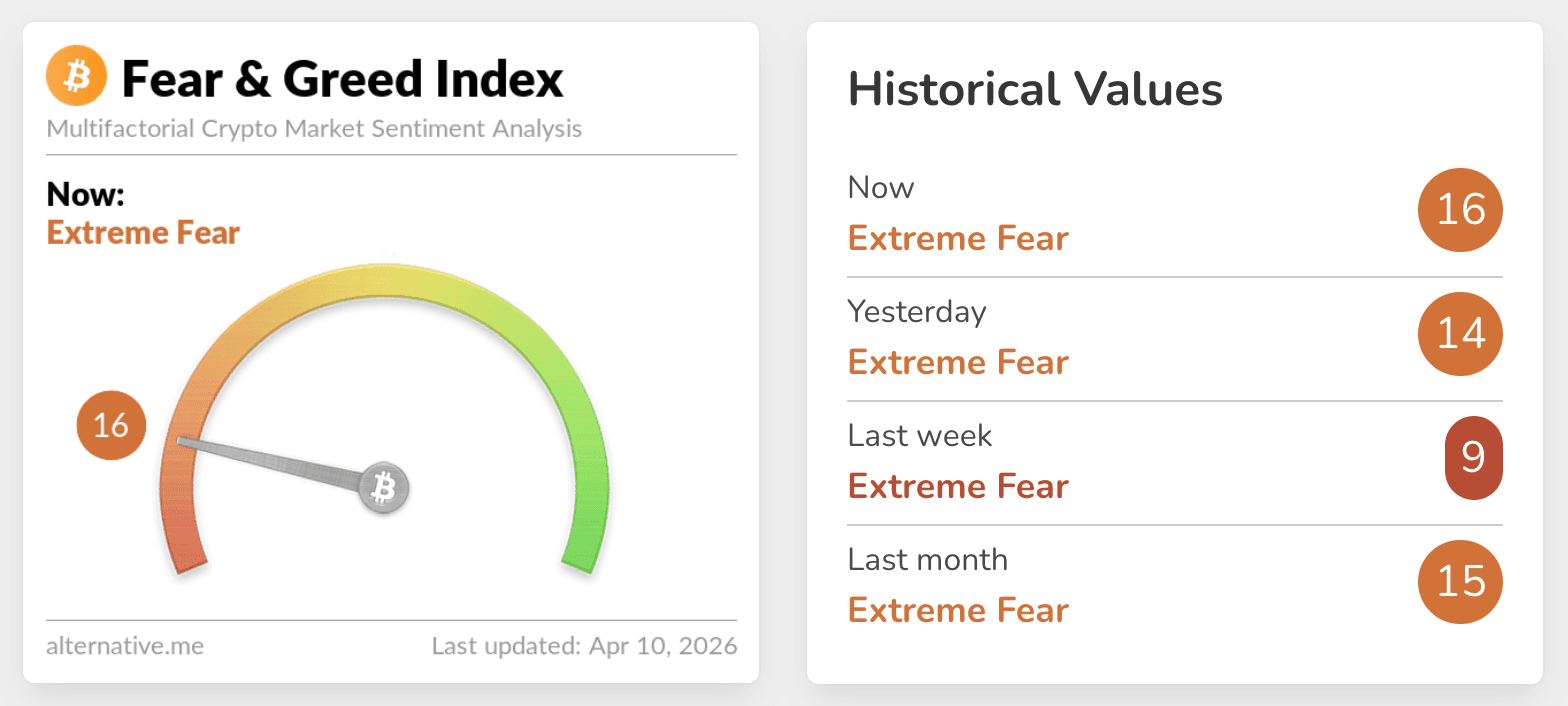

The Crypto Fear & Greed Index currently stands at 16, which still places the market in Extreme Fear. This shows that although prices recovered today, broader long-term sentiment remains cautious. In terms of price action, Bitcoin (BTC) briefly touched an intraday high of $73,145 this morning before consolidating around the $72,000 level, with a 24-hour gain of about 2.01%. Ethereum (ETH), meanwhile, hovered near the $2,200 level and posted a gain of around 0.91%. From a trading cost perspective, BTC’s average eight-hour funding rate across the market stood at -0.0024%, indicating that hedging activity or short positioning is still present. ETH’s average funding rate stayed slightly positive at 0.0013%. According to liquidation heatmap data, if BTC drops below $68,234, major CEXs could face around USD 2.093 billion in long liquidations. On the upside, a break above $75,344 could trigger USD 1.127 billion in short liquidations. For ETH, the key support and resistance levels stand at $2,081 and $2,296, with corresponding liquidation clusters of USD 955 million and USD 705 million. This suggests that a large amount of leveraged positioning has built up within the current range, and short-term volatility could expand further once those liquidation zones are tested.

Source: Alternative

Key News Highlights:

CIA Plans To Integrate AI Co-Workers To Improve Intelligence Analysis And Counterintelligence Capabilities

The US Central Intelligence Agency recently said it plans to embed “AI co-workers” directly into all of its analytic platforms within the next two years. According to CIA Deputy Director Michael Ellis, these tools will help analysts detect spies and anticipate hostile moves by foreign adversaries. The system is described as a classified version of generative AI and is intended to assist intelligence officers with basic tasks such as drafting key judgments, testing analytical conclusions, and identifying trends in intelligence gathered from abroad. While AI is expected to take on a growing share of data-heavy work, the agency stressed that humans will continue to make the key decisions. The initiative comes as the US government remains in conflict with Anthropic over restrictions on the use of its technology in sensitive defense and surveillance contexts. Against that backdrop, the CIA has argued that it cannot allow the preferences of a single company to constrain national capabilities. The agency also revealed that it tested around 300 AI projects last year, including use cases in language translation, large-scale data processing, and report generation. Ellis also emphasized that blockchain transparency has strategic value for counterintelligence work, adding that the CIA continues to monitor technological competition in the crypto sector to ensure the United States remains well positioned against China and other adversaries.

Bitcoin Rally Extends Toward $73K Despite Weak US Economic Data And Geopolitical Volatility

Bitcoin reclaimed the $72,000 level despite data pointing to rising inflation and weak economic growth in the United States. Recent macro releases, including a downward revision of fourth-quarter GDP growth to 0.5%, have reinforced concerns that recession risks are rising. Yet that same backdrop has also supported the appeal of scarce financial assets. Market participants increasingly appear to believe that if economic weakness deepens, policymakers may eventually be forced to inject more liquidity to support markets. That shift in expectations has weighed on the US dollar, with the dollar index slipping to 98.819. On the geopolitical front, oil prices climbed back toward the $97 range after senior Iranian officials accused the US and Israel of violating the ceasefire, raising fears that risk markets could come under renewed pressure. Even so, Bitcoin continued to show resilience and remained closely aligned with the broader tone in equity markets. Rather than reacting to weak macro data with outright risk reduction, traders appear to be balancing recession concerns, inflation protection, and the prospect of future liquidity support. Although the fragile truce and rising oil prices may limit Bitcoin’s upside in the near term, the current move suggests that the asset is still benefiting from demand for scarcity in an environment marked by a weakening US dollar and rising uncertainty around fiat purchasing power.

Distributed Tokenized RWA Market Projected To Reach USD 400 Billion By 2030

According to a new joint report from market maker Keyrock and tokenization platform Securitize, the distributed tokenized RWA market, meaning tokenized assets that are freely transferable on-chain, is projected to grow from around USD 29 billion today to USD 400 billion by 2030 in the base case. That would mark growth of more than 1,000%. The report identifies perpetual futures as the fastest-growing on-chain channel for RWA exposure, particularly for assets tied to gold, silver, and oil. Trading activity in these products has expanded sharply, with RWA perpetual volumes rising 40x in six months to USD 67 billion in monthly volume. Their share of total on-chain derivatives volume has also climbed from 0.1% to 10.1% since October 2025. If that pace continues, the report projects RWA perpetuals could account for 50% of all on-chain derivatives volume by 2028. The report also highlights strong institutional interest in tokenized US Treasuries. Since mid-2024, tokenized T-bills have delivered yields above DeFi’s benchmark stablecoin lending rate on 64% of all trading days, while yield volatility has remained significantly lower. Keyrock and Securitize identify 2027 as a likely convergence window, when regulation, liquidity infrastructure, market depth, and distribution channels may mature at the same time. In that scenario, RWAs would move beyond simple on-chain wrappers and become a more foundational part of the DeFi ecosystem.

Trending Tokens:

Anichess has officially launched Season 7 Gambit, introducing a direct wager system that marks a major evolution for its blockchain chess ecosystem. In this format, each player must stake 100 $CHECK per match as an entry fee, while the total prize pool for the season exceeds 1,000,000 tokens. Participants will compete for positions on the weekly Gambit leaderboard, and the top 50 players by total weekly volume will share 250,000 $CHECK. To lower the barrier to entry, the project introduced a loss protection mechanism in the first week, offering a 25 $CHECK refund for each match. This season also includes designated peak hours with double leaderboard points, designed to maximize liquidity and player participation during specific time windows. In addition, the multi-tier referral system and the M8 Arena reward track provide players with extra ways to accumulate assets. This strategic update highlights skill-based competition while leveraging the Abstract ecosystem to enhance player rewards and overall performance.

Market activity around the SOON Network surged after it announced a second round of airdrop rewards through a major exchange’s Alpha program. Users who meet the minimum score threshold can claim 280 $SOON tokens on a first-come, first-served basis. This distribution model uses a dynamic score requirement that automatically decreases every five minutes, helping improve reward pool allocation efficiency. Built as an SVM-based rollup stack, SOON is designed to deliver high-performance scalability and interoperability for a wide range of Layer 1 blockchains. Its architecture, known as the Super Adoption Stack (SAS), includes core components such as the SOON Mainnet and InterSOON to support seamless onchain interaction. Strategic integrations with platforms such as Twitch and SOOP are intended to narrow the gap between Web2 environments and decentralized infrastructure. This approach positions SOON as a critical infrastructure provider for high-traffic applications that require a robust and interoperable execution environment.

Unitas Labs has successfully raised USD 13.33 million in seed funding to build an infrastructure layer for sustainable onchain yield generation. The round attracted participation from prominent institutional investors, including Amber Group, SevenX Ventures, and Bixin Ventures. By implementing a transparent and market-neutral execution framework, the protocol aims to address structural challenges such as yield compression and strategy opacity. Unitas offers a range of yield-bearing assets, including stablecoins and tokenized commodities, supported by institutional-grade risk management and monitoring systems. This infrastructure is designed to serve as a unified settlement layer that can help institutions enter decentralized finance with greater transparency. The new capital will be used to expand strategy development and bring a broader range of real-world assets into the ecosystem.

Disclaimer: The information provided in this section is for informational purposes only and doesn't represent any investment advice or FameEX's official view.